Using floating rate debt to finance multifamily projects is commonplace, unremarkable really—until it isn’t.

With rising rates, an inverted yield curve, and wider spreads, getting or keeping variable rate debt on multifamily projects is becoming more difficult.

The CRE landscape is ripe for cash flow havoc.

A typical bank construction loan or mini-perm is priced based on the Secured Overnight Financing Rate (SOFR) plus a spread. As the Fed has raised rates, SOFR has risen too. A year ago, SOFR stood at 0.79%. As of this writing, SOFR is 5.06%. Spreads are widening, too. Loans that were priced at 150 or 200 basis points over SOFR a year ago can price today at 300 over or more. Increases of that magnitude play havoc with construction loan interest reserves and can quickly push cash flow negative, even on otherwise healthy operating properties.

Interest rate caps only add to the complexity.

Of course, lenders and developers can choose to hedge interest rate risk with caps. Fannie and Freddie require borrowers to purchase interest rate caps for the loan term or until the date of a permitted conversion to a fixed rate. What was once a backstop or just another cost of doing business is now out of reach for many borrowers and deals. Depending on the deal size, strike rate, and term, caps that once cost tens of thousands of dollars can now add millions to the cost of a project.

Remove the risk with FHA financing.

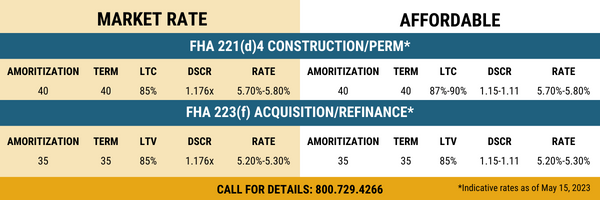

FHA financing for multifamily can be an excellent alternative to floating rate debt. With lower debt service coverages (DSCs) and longer amortization and terms (35 years for a refinance and 40 years for new construction), FHA can offer more proceeds on a given deal and eliminate both interest rate and refinance risk.

.jpg?upscale=true&width=1200&upscale=true&name=Normal%20Dial%20(1).jpg)